Bookkeeping is the backbone of any small business. Proper financial management ensures your business stays compliant, informed, and positioned for growth. However, many small businesses unknowingly make bookkeeping mistakes that can lead to costly errors, penalties, and even lost opportunities. Here are ten common mistakes and how you can avoid them.

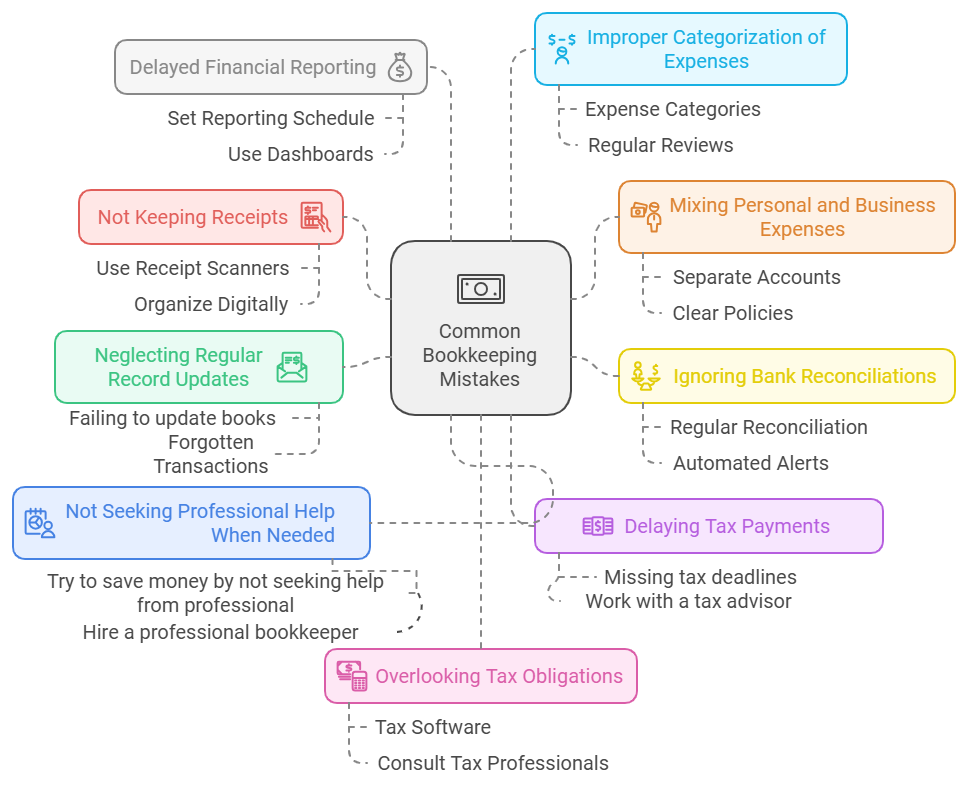

1. Mixing Personal and Business Finances

The Mistake: Many small business owners use the same bank account or credit card for personal and business transactions, which creates confusion during tax season and financial analysis.

How to Avoid: Open a dedicated business bank account and credit card. This separation makes tracking expenses easier and ensures cleaner records.

2. Neglecting Regular Record Updates

The Mistake: Failing to update books regularly can lead to forgotten transactions, incorrect balances, and incomplete financial statements.

How to Avoid: Set aside time weekly or bi-weekly to review and update your books. Use accounting software with reminders to stay consistent.

3. Skipping Expense Categorization

The Mistake: Improperly categorizing expenses or lumping everything into “miscellaneous” can lead to inaccurate financial reports.

How to Avoid: Create a clear chart of accounts tailored to your business needs. Use bookkeeping tools that automate categorization based on transaction details.

4. Ignoring Small Transactions

The Mistake: Dismissing small transactions as insignificant can add up to big discrepancies over time.

How to Avoid: Record every transaction, no matter how small. A habit of thoroughness prevents errors and builds accurate records.

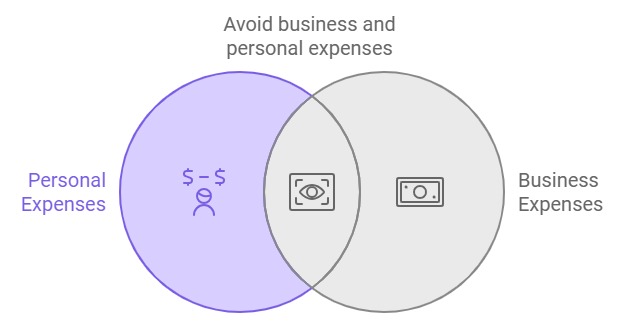

5. Not Reconciling Accounts

The Mistake: Failing to reconcile bank accounts regularly can result in undetected errors, duplicate entries, or missing transactions.

How to Avoid: Reconcile your accounts monthly. Compare your financial records to bank statements to identify and correct discrepancies promptly.

6. Overlooking Tax Deductions

The Mistake: Many small businesses miss out on allowable tax deductions because they don’t track eligible expenses.

How to Avoid: Keep detailed records of business expenses and consult a tax professional to ensure you’re claiming all eligible deductions.

7. DIY Bookkeeping Without Proper Knowledge

The Mistake: Attempting to handle bookkeeping without understanding the basics can lead to errors and compliance issues.

How to Avoid: Invest in training, hire a professional bookkeeper, or use user-friendly accounting software to manage your books correctly.

8. Failing to Keep Receipts

The Mistake: Not keeping receipts can make it difficult to validate expenses during audits or when claiming deductions.

How to Avoid: Use digital tools to scan and store receipts, making them easy to access and organize.

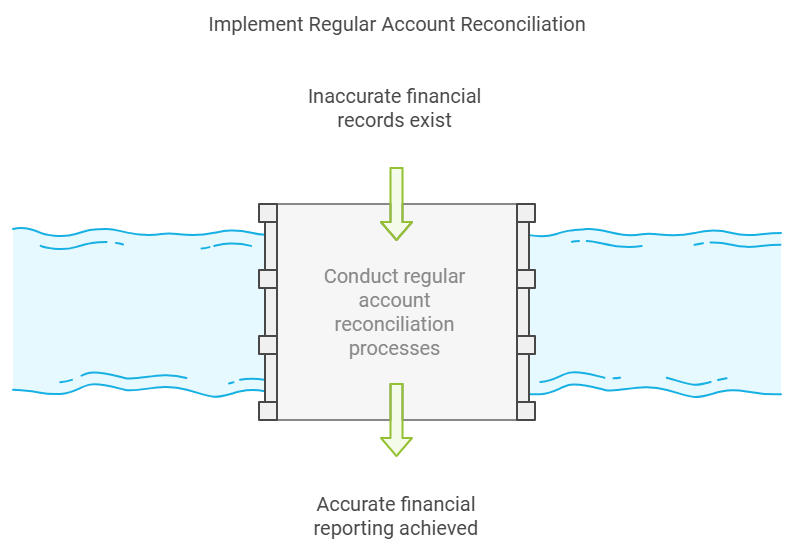

9. Delaying Tax Payments

The Mistake: Missing tax deadlines or underpaying taxes can result in penalties and interest charges.

How to Avoid: Mark tax deadlines on your calendar and set reminders. Work with a tax advisor to estimate and pay quarterly taxes accurately.

10. Not Seeking Professional Help When Needed

The Mistake: Trying to save money by avoiding professional help can lead to costly mistakes down the road.

How to Avoid: Know when to delegate. Hire a professional bookkeeper or accountant to handle complex financial tasks and ensure accuracy.

Conclusion

Avoiding these common bookkeeping mistakes can save you time, money, and stress, allowing you to focus on growing your business. If you’re unsure about handling your business finances, outsourcing to a trusted bookkeeping professional can be one of the best investments you make.